Basic Accounting Concepts for Small Business Managers

For a small business manager it is important to understand some basic accounting concepts that can help to manage the business. These concepts include, debit, credit, business documents like invoices, delivery note, debit note, credit note, financial reports, tax compliance, tax planning, financial analysis, taxes and other aspects that are related to accounting and business management. In this article, we will explain these basic accounting mechanics that can help to manage your business.

Accounting starts with the basic knowledge of a debit and credit. As a rule of thumb, an increase in an asset is a debit and an increase in equity and liability is a credit on the balance sheet. If you purchased an asset on credit, then it is an increase of assets along with the increase of liability. This double entry can be shown below.

| Particulars | Debit | Credit |

| Asset (debit) | XXX | |

| Liability (credit) | XXX |

Since for this entry, an asset has been increased, the debit impact is increased. On the other hand the credit impact is reflected in a liability as it has also increased in the same transaction.

This given entry only impacts the balance sheet as there is no revenue or expense in the transaction. If, however, there is a revenue and expense, this is recorded through the profit and loss statement.

Next we will explain how a revenue and expense is recorded.

As a guideline, an increase in revenue is a credit and an increase in expense is a debit. Just say that you make a sale amounting to $10,000 and expenses amounting to $7,000 (all receipts and payments are in cash). This entry can be recorded as:

(For recording revenue)

| Particulars | Debit | Credit |

| Cash (debit) | 10,000 | |

| Revenue (credit) | 10,000 |

The debit impact of this transaction is the receipt of cash. This is because cash has been received. The credit impact of the transaction is that revenue has been credited, as it has been increased.

(For recording expenses)

| Particulars | Debit | Credit |

| Expense (debit) | 7,000 | |

| Cash (credit) | 7,000 |

The debit impact of this transaction is recording for the expense. This is because an increase in an expense is recorded as a debit. On the other side of the transaction, a credit is recorded since this is a cash payment received.

At the end of the accounting period, all the entries for the revenue and expenses are closed in the balance sheet. If there is a profit, which is when revenue is more than expenses, then this is recorded as an increase in equity. If there is a loss, where revenue is less that expenses, then this is recorded as a decrease in equity.

In our example above, the revenue was for $10,000 and expenses amounted to $7,000. This means the profit is $3,000 ($10,000 - $7,000). This will be recorded as an increase in equity (retained earnings) at the time of the closing of the accounting period. If entries are recorded in the profit and loss statement, the net impact of the profit or loss is taken to the balance sheet (equity). So if there is a profit, then equity increases and vice versa.

It is important to mention that entries should only be posted to the books, if the transactions are backed by appropriate source documents. If for example sakes, that you purchase inventory and intend to post the entry into the accounting book. This should only be done once you have actually received the goods. To prove the receipt of goods, a delivery note and supplier invoice should be attached to prove the transaction took place and for audit purposes. Next we will discuss what is a delivery note and invoice.

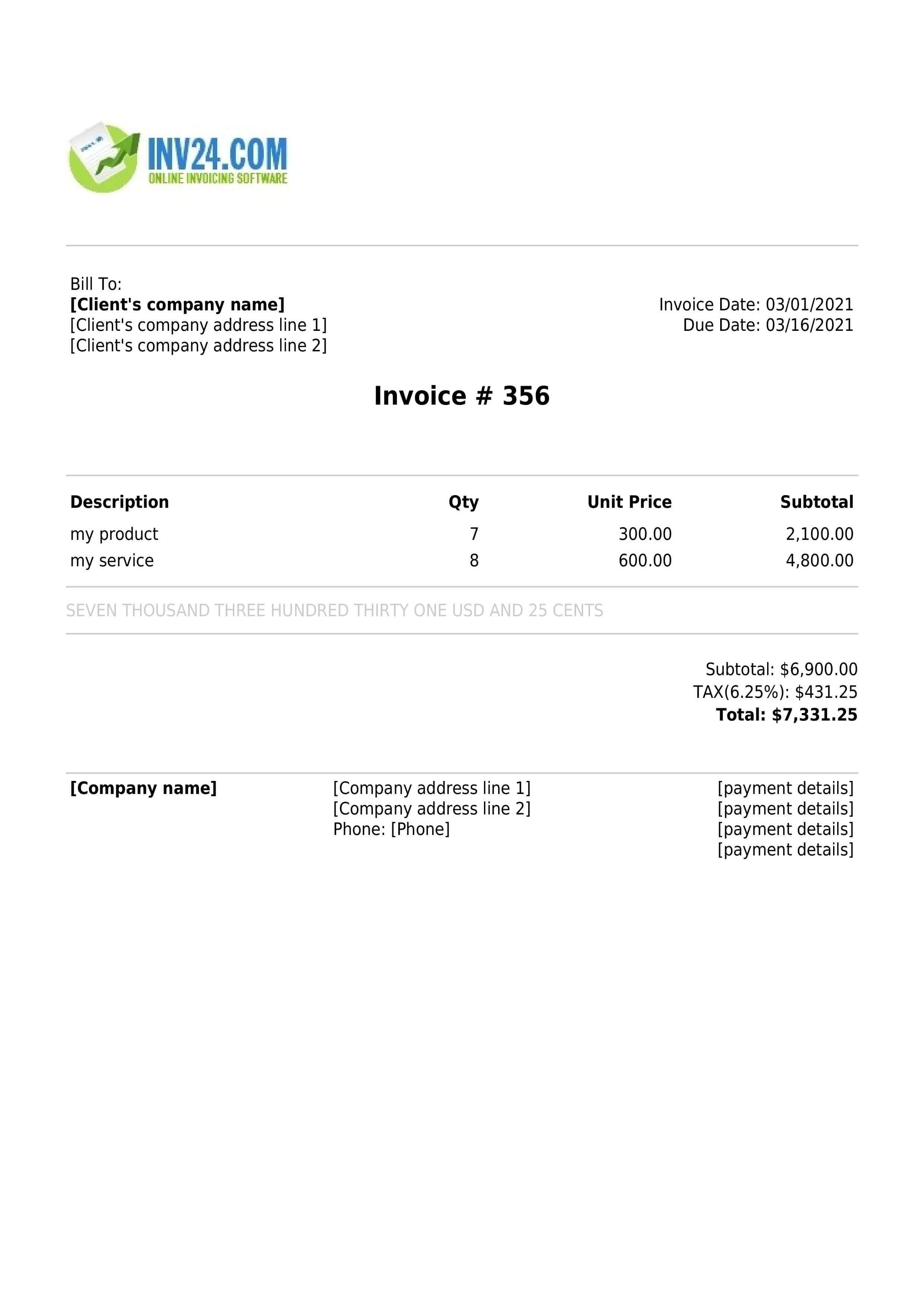

What is a Delivery Note and Invoice?

A delivery note is a paper note that is prepared once a business has received goods. It contains the quantity as well as description of goods that have been received by the business and a copy of this delivery note is also sent to the supplier. It is also good practice to have the note attached to the invoice to ensure that you only paid for the goods that have actually been received.

For instance, on a delivery note, there are 10 units of product A. However, on the invoice, the supplier has detailed that there are 12 units of product A. This means that you have actually received 2 less units of product A than what was on the invoice. So you will need to file a grievance that you have received 10 units but had been invoiced for 12 units. Like this example, it is important to understand how these two documents work together.

An invoice is a bill that is sent from the seller to the customer that details the goods purchased. It acts as a request for payment and is sent when the goods have been delivered to the customer. On the invoice, details that are included are product description, quantities, agreed prices and other related details of the transaction.

It is also important to note that the quantities of the products or services that are detailed on the invoice is reconciled with the details on the delivery note. Similarly, the rate on the invoice needs to be reconciled with the purchase order which is a form that was originally placed with the supplier to purchase certain goods. This is to make sure that correct amounts of goods were sent and received.

All of this points to the fact that details of purchase transactions need to be reconciled with documents such a purchase orders, invoices and delivery notes. The purpose of the reconciliation is to ensure the accuracy of the transaction as all of the documents are prepared at different times of the transaction cycle.

There may also be a need from time to time, to prepare and issue specialised documents such as debit notes and credit notes while doing the accounting. Next will be a discussion on what these documents are used for and how they help in accounting.

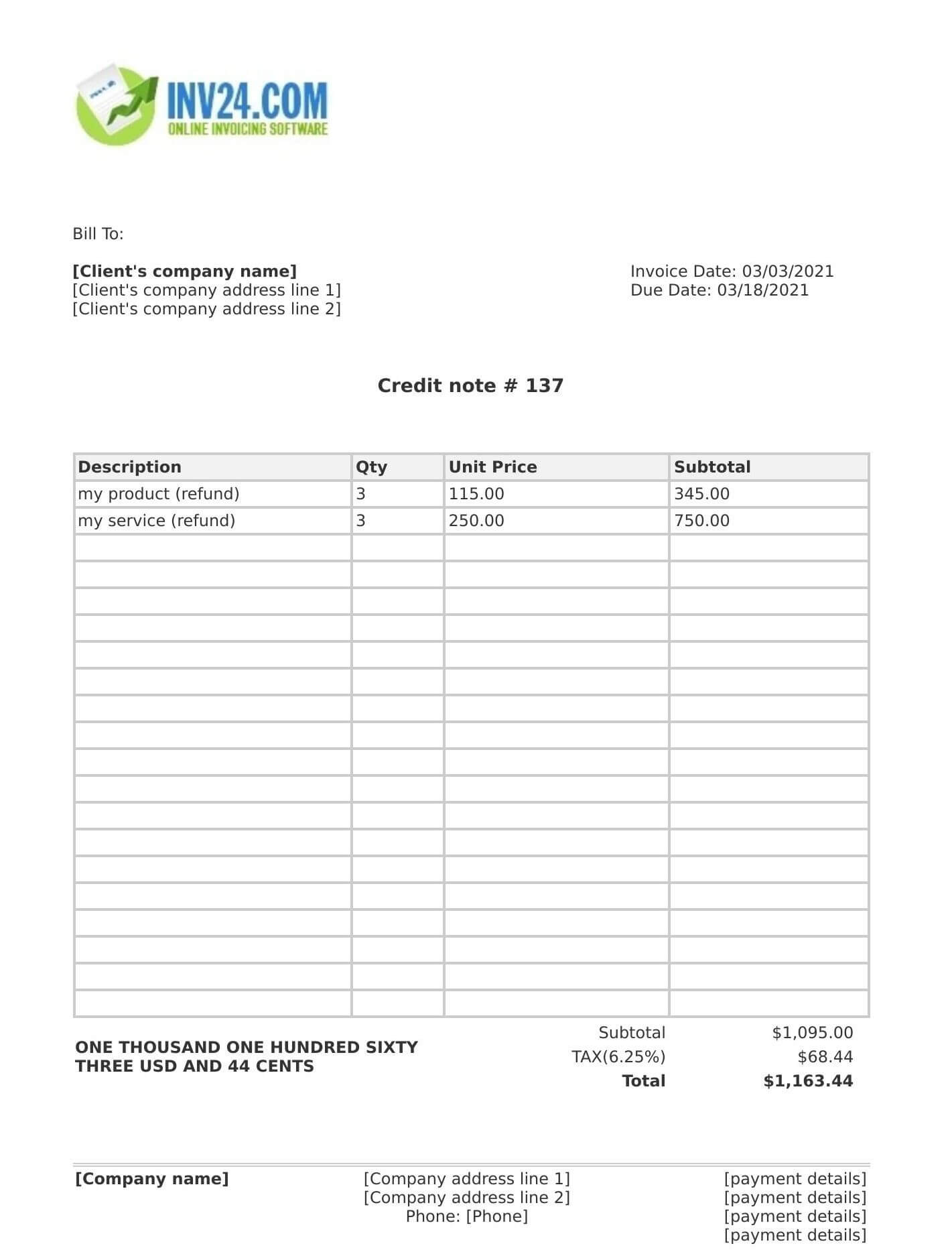

What are Credit Notes and Debit Notes?

A credit note leads to a reduction in the accounts payable balance. This document is sent by the seller to the buyer where there is a need to cancel a complete or portion of an invoice. This document is used to communicate to the buyer or customer that the balance that is to be paid, will be reduced.

On the other hand, a debit note is produced by the buyer and is sent to the seller and it communicates to the seller that the customer has returned the goods. This then reduces the receivables balance of the seller.

Documents such as invoices, debit notes, delivery notes, and credit notes act as source documents that build up accounting records and provide proof of the transaction. Once the accounting period is complete and all the transactions are posted in the accounting system, then the books will be closed and a financial statement will be prepared.

Of note, there are two types of entries in the accounting books. The first is what is known as operational accounting entries. These types of entries are posted on a day-to-day basis. So, if for example you earn revenue, you will need to record it. The second type of entry is related to closing of the accounting period. For instance, if you make use of equipment in the business, there is a need to record depreciation at the end of the accounting period. These types of entries are periodic. Similarly, there is a need to adjust the prepaid balance at the time of closing.

Once all of the entries are posted in the accounting books, there is a need to close the books and then prepare a financial statement. The step after is to combine the net balances of all ledgers and produce a trial balance. At this stage, it is imperative to make sure that the debit and credit of the trial balance is equal. Then after the trial balance, there is need to map the figures and balances. At this stage, you will have a good understanding of each balance in the trial balance and can therefore map accordingly. For example, if it is an asset balance, then there is a need to map in the codes that fall on the asset side.

You may also need to adjust the balances and provide provisions. It is important to remain alert about each and every transaction so that you will be able to calculate correct balances and produce accurate financial statements.

For analysis purposes, the calculation of profit and loss does not end here. In fact, financial analysis begins once the profit or loss has been calculated. You can opt to compare profit and loss for a particular period with corresponding periods to see if the business has been improving or not. Similarly, ratio analysis can be undertaken to give a good understanding on how any business aspect can be improved upon.

For example, you can calculate profitability ratios, gearing ratios, liquidity, solvency and valuation among others. You might find that your business is good in one area and weak in another. So there may be a need to find balance. For instance, your business may be profitable, yet you are struggling with liquidity. In this situation, you may need to offer a cash discount and improve your liquidity position. This is why ratio analysis can help in decision making and effective business management.

Once the financial statement is final, the next stage is to pay tax. Tax planning actually starts from the very first day. Tax planning means setting a financial plan that leads to the lowest tax liability that is legally possible. It involves appropriately using tax allowances, making investments in tax-friendly schemes, planning for the time of expense and allowance and so forth. The whole process of tax planning needs to be undertaken throughout the entire accounting period, put simply, from the beginning to the end. Tax compliance means ensuring the tax laws are fulfilled and abided by. If a business does not comply with tax laws, it may lead to penalties and interest charges.

In addition, if you are registered for sales tax, there will be a need to maintain ledgers for the sales tax payable and sales tax receivable and the calculation of taxes. The next section of this article will describe how this is done.

How to Calculate Taxes

If your business is registered for sales tax, then you will be required to collect tax from customers. This needs to be collected when invoicing the customer. Furthermore, the tax collected needs to be shown as a liability as this money does not relate to you, in fact it must be submitted to the government. However, you can adjust the tax that you have paid on the purchases. If you have collected more tax on sales than the tax paid on purchases, then you are required to record this as a liability and pay the government tax authorities. If you have paid more tax on the purchase than collected tax, then you will be able to receive a refund that will be collected from the government.

In order to have less chance of errors and also to ensure that things remain in control, it is advisable to maintain a separate ledger for the sales tax and ensure that all input tax (on purchases) and output tax (on sales) are recorded appropriately.

There can be a lot of complexity and difficulty in controlling accounting functions. There may even be more difficulty in tracking figures, balances as well as ensuring the appropriateness of the accounting record. This is why it is a good idea to implement accounting software as well as appointing a professional accountant.

Accounting software can help with the business as there is higher integration flexibility and an overall increase in the execution of accounting responsibilities. Also, a professional accountant can help to enhance the overall credibility of the accounting function. We now turn to explaining how to appoint a good accountant for your business.

Conclusion

It is important to understand basic accounting concepts in order to run a successful business. As a good business owner, it is ideal if you can understand the nature of transactions and classify them in the appropriate place in the financial statement. As mentioned above, there are two crucial aspects in accounting. The first being the actual preparation of financial statements and the second is to keep an appropriate record of the accounting transactions. Once profit has been calculated, there is need to analyze financial figures and calculate taxes.

Frequently Asked Questions

Does equity increase if there is a profit in the income statement?

The answer to this question is “yes”. The net equity increases if there is a profit in the income statement. This reflects the fact that profit is earned by the business and is closed in the balance sheet. Hence, equity increases when there is profit. If there is a loss, then the net equity will decrease.

What is an invoice generator?

An invoice generator is a software that allows the generation of an invoice in just a few clicks. To use this, you will need to input data in relation to your business and the customer details, such as invoice amount and address and the rest of the work is performed by the software.

Accounting tools for small business: